April 2022 Market Report for Palm Beach County – Presented by Amy Snook

Palm Beach County April 2022 real estate market report highlighting the changes that are being seen due to rising interest rates, leveling off of pricing, but does include lots of good news for sellers and buyers alike.

No one has a crystal ball as to what the future will hold for Palm Beach County real estate but while you can feel a shift in the frenetic energy that consumed our market for the past several years, there is no denying that demand is still strong for our market.

So what does that mean for us Palm Beach County Residents? Lets look at the April report showing March 2022 final numbers.

First, similar to last months’ report, under $999,999 is still a strong seller’s market showing 2 months of inventory – versus a balanced market which is typically 5 to 7 months of inventory. Over one million is holding steady for several months now at 5 months of inventory – just on the cusp of a more balanced market. These results of course take into account closed sales which were under contract earlier in the year and so the next few months will be important as we continue to analyze the market.

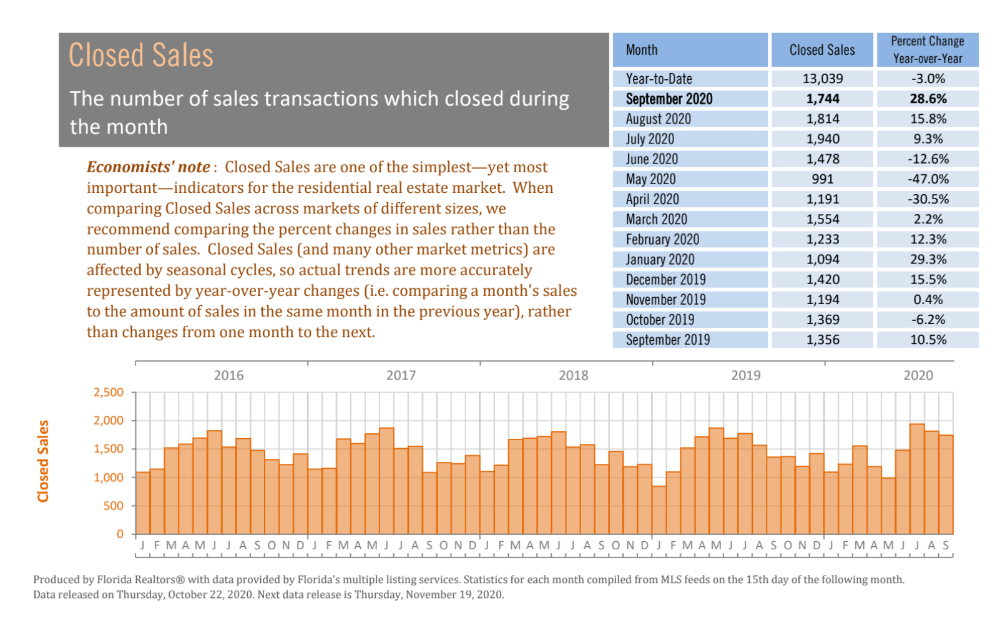

Now, what’s different this month than the past few months of our market report? Several factors, closed sales and pending sales are both down from the same time last year- this is no surprise when you look at the fact that the sense of urgency to relocate to south Florida has waned slightly and mortgage interest rates are up. Interestingly while total volume of closed sales is up due to the higher price per sale, in Palm Beach County our median sales price is up 23% while our average sales price is down 7.1% – as we have shared in the past the differential between median and average is great in our Palm Beach market due to the sheer number of higher end homes we have in our county versus other counties.

Also watching our multiple listing service we are starting to see price reductions more frequently than we have over the past few years when listings came and went under contract before you could even say the word “listing”. Now personally, I don’t necessarily feel this is 100% indicative of a slowing market but rather shows that the listing prices of many new homes going on market are not taking into account everything that is going on in the market and in the world. Our listing prices are not increasing at the rate in which they were over the past several years.

Our advice, be aggressive yet realistic and strategic on your list price. When we meet with Seller’s, we review the active comparables, your competition, pending, what is selling and then closed over the past 90 days or so. Important to also note is what someone can buy at the targeted price point – there aren’t a lot of options for buyers therefore looking at the entire picture together, Listing Agent and Seller (s), to make the pricing decision. Thank Goodness, marketing once again matters.

We are fortunate to have a higher demand than most areas around the country – buyers want to relocate to our area full time, want a second home or even just a seasonal vacation home. A balanced market is good for us all so while the numbers showing a decrease year over year can be concerning, in this case, I would say it is a sign of our real estate market heading towards a more stable market for both buyers and sellers alike.