November 2023 Market Report – By Amy Snook

![]()

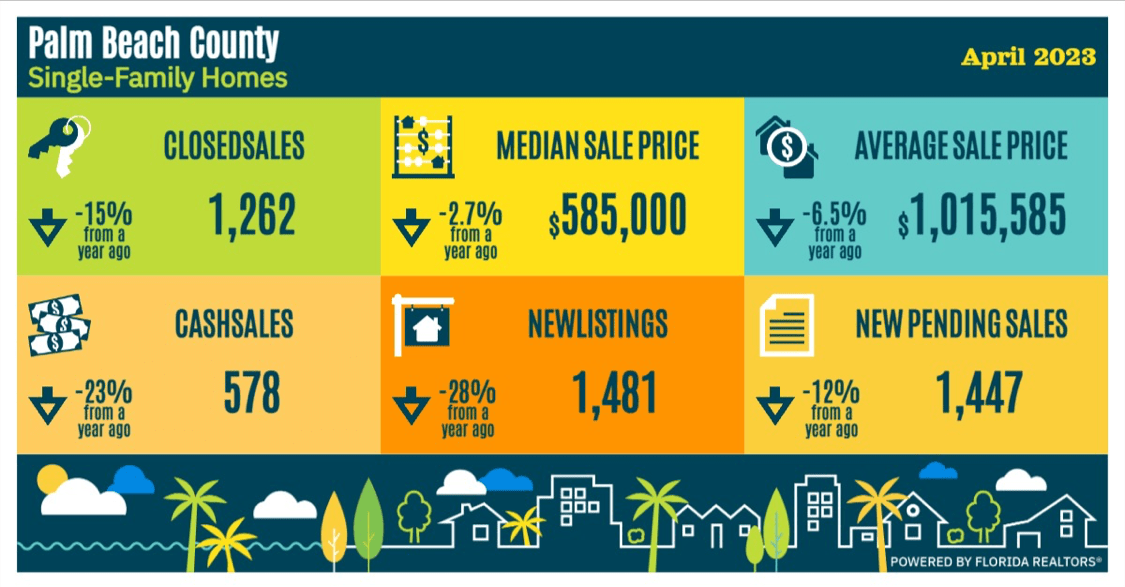

November 2023 Market Report – October 2023 Data

Our phone has been inundated with inquiries following the recent news release highlighting a significant drop in pending sales, marking the lowest figures in many years. The reports suggest a return to a Seller’s market due to inventory dwindling to 3.2 months, well below the threshold for a balanced market.

However, it’s crucial to recognize that the media’s portrayal is just a snippet of the whole narrative. While their statements may hold some accuracy, they fall short of capturing the complete picture, much of which is positive. I urge caution in accepting media reports as absolute truth. Feel free to reach out to us at any time, allowing us to provide a comprehensive understanding of the real dynamics in our market.

Certainly, pending sales saw a decrease but of only 97 homes in Palm Beach County compared to the previous month (1034 down from 1131). Yet, when considering the same period last year, a more seasonally relevant metric for our market, there is an increase. New listings entering the market have also risen by 11.4% from the corresponding time last year.

Nationally, people have been in a holding pattern, monitoring interest rates, the stock market, and global events. A recent drop in interest rates, coupled with the acknowledgment that these rates are our new reality, has spurred Sellers to act. This might not be universally true, but in our Palm Beach County market, a sought-after destination, the situation is more optimistic than the news suggests.

Cash sales have seen an uptick, our median sales price is on the rise, and although the average sales price has dipped, it’s attributed to the luxury market’s slower pace compared to price points under $1,000,000. Consequently, we now have 10 months of inventory, classifying it as a buyer’s market. However, price points below $1,000,000 remain in the Seller’s market territory with inventory below the 5-7 month range considered balanced.

Despite the prevalence of luxury homes skewing the average, our local real estate market is far from doom and gloom. We’re actively listing and selling homes, employing creative contracts with seller concessions, innovative marketing strategies, and increased investments in open houses and broker events. The palpable surge in activity and enthusiasm in the South Florida market indicates an upward trend, and I eagerly anticipate next month’s report reflecting the impact of our seasonal dynamics.

Amy