How Do Agents Qualify A Buyer?

A seller asked Noreen and Amy how they will know buyers who viewed their home is qualified to buy. Great question. Get the answers here!

A seller asked Noreen and Amy how they will know buyers who viewed their home is qualified to buy. Great question. Get the answers here!

Ever wonder how we find the right home for our buyers? Noreen gives you an inside peek into her tried-and-true process in this short video. She explains how she helps her buyers hone in on the neighborhood and the home that is just right for them!

Is it better to choose a home with an HOA (homeowners association), or one without and HOA? Noreen reviews some pros and cons and offers some help with making this personal decision.

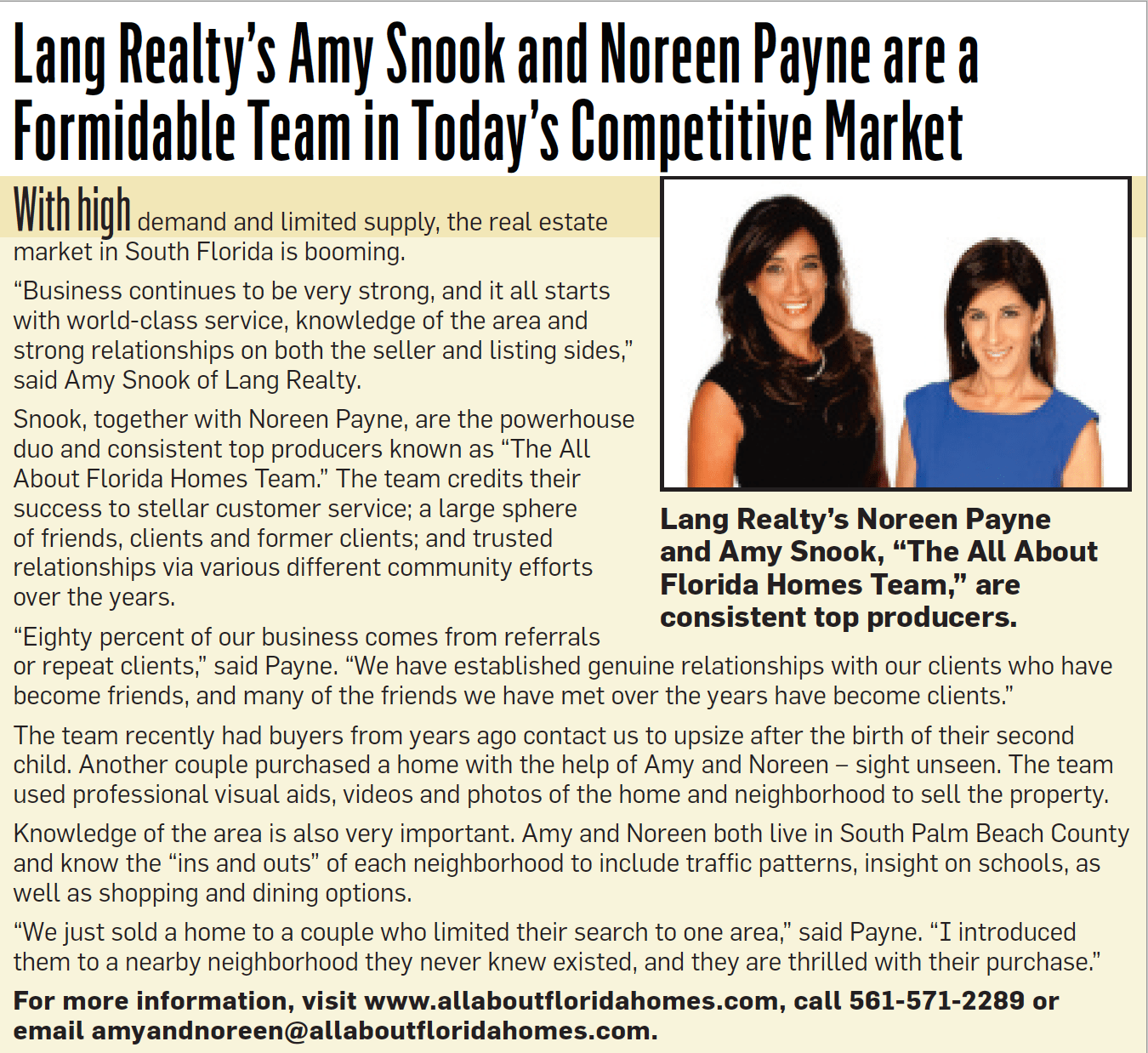

It’s the same ol’, same ol’ this month in the South Florida real estate market.

Once again, a low inventory of listings and an abundance of would-be buyers continues to make it a red-hot sellers’ market.

How will the forecast of increased interest rates change that, if at all? How will the war in Ukraine affect the U.S. real estate market, if at all? And now that America seems to be finally emerging from the Covid-19 shutdowns, will the influx of buyers into our Palm Beach County market continue?

These are questions that we are being asked daily from our clients and friends and while none of us have a crystal ball, we do feel our years of experience will help provide some insight.

Every month, we created a spreadsheet and conduct an analysis of the numbers of our market versus the rest of the state.

For example, our market is unique and usually differs from the reports summarizing the rest of the state and other price points across the nation. If you watch the local news, or follow real estate reports, a one-month inventory of the state lists a median sales price of $350,000. Palm Beach County’s median price, however, was $526,000 in January and our average price was $826,000. The huge differential is due to the number of seven-figure homes for sale which we have in Palm Beach County.

For those new readers to our report, understanding “months of inventory” is crucial. That term means a hypothetical that if no new homes were added for sale, how long would it take for every home for sale to be sold?

The statewide average inventory in January was one month, but in Palm Beach County homes under $999,999 is two months, but for over-$1,000,000 it has increased from December to January from three to five months, which was a needed increase toward a more balanced market.

Our Palm Beach market still attracts many new homeowners seeking our beautiful winter weather and outdoor lifestyle. Thousands more employees are working from home these days, which means they are free to relocate but still hold the same job. Also, thousands more are buying second homes in South Florida. We do not see this slowing down any time soon.

Some say that the market is softening when they see a price reduction in a home.

However, to us that just meant that agents had overpriced the homes to begin with. They were overpriced, even in today’s terms, and sat on the market. If you price your home right however, it will attract a buyers’ frenzy.

So, what does our future hold?

We believe that the upcoming increase in interest rates will have only a moderate impact in our market – mostly with the lower price points. But on $800,000 homes and above, we will continue to see mostly cash transactions. In fact, in January, there was a 30 percent increase in cash transactions from the same time a year ago.

We will have would-be buyers find properties — and emerge as the actual buyer should a bidding-war ensues against others who want the same home. And that is happening now more than ever. Should you want to sell and take advantage of this super-hot market, we also know how to price and market your property effectively to capitalize on all these factors.

We would love the opportunity to discuss your personal situation and what is best for you.

With the highest medium and average sales prices that we have seen in over a year and inventory weighing in at record lows, April 2021 rang in an unprecedented time in real estate. A surefire indicator of market conditions, 6-9 months of inventory is considered a balanced market. Under 6 makes for a Seller’s market, and over 6, a Buyer’s market. The average inventory in Florida today across all price points is 1.8. That’s right, a mere 1.8! Never fear, however, hope isn’t lost for the motivated buyer in Florida.

Whether you’re a buyer or seller, this market calls for strategy. To approach real estate with a recipe for success, you must account for the ingredients at hand.

Here’s the bread and butter of it: cash sales are up significantly in Palm Beach County, according to the April 2021 Florida Realtors report. It’s important to remember “cash sales” doesn’t always mean green: but instead, that the transaction was not contingent upon financing.

So, for our seller’s out there: you’ve got high probabilities of a cash offer coming your way. Now, does this mean you shouldn’t accept a finance offer? Not in the least! It means that Sellers are empowered to “demand” certain elements should you accept a mortgage. Such as a quicker loan commitment— meaning the contingency for finance ends faster (including appraisal and loan conditions). You can also weigh your options on whether to allow an appraisal contingency— for the right buyer, omitting this step may suit just fine, and the finance offer can move forward.

As for buyers? It’ll be key to keep in mind that you’re competing against cash offers— so offers need to be written aggressively, and with the least amount of contingencies. That said, it’s important to ensure you’re protected as well; and in that, a good agent will make all the difference.

Now factors aren’t the same across all price points. April’s market sweet spot is the $400-599k price point. In this turf, homes are selling in a stunning 8 days. That, compared to the 1,000,000 plus market, which is an average of 27 days to contract. So if you’re selling a home at $500,000, your price is right, the place is properly staged, and sports curb appeal? Well, you’d better start packing!

Buyers—I’m sure you’ve read your fair share of stories on scarcity, that homes just can’t be found. We’re here to tell you that they absolutely can! Simply put, you’ll need three tricks to compete in this market: an aggressive offer, the preparation to write it quickly, and a partnership with the right agent who has your back and your interests in mind.

Sellers— are you scared to sell because you haven’t yet pinned down where you’ll go next? Not to worry, we have a plan for that. Let’s partner up to sell your home and gain you the most we can, while holding space for a strategy that allows you time to find the right home for your needs. It’s a Seller’s market out there, and you’re in the driver’s seat for both your sale AND your purchase. Sit down with Noreen and I of the All About Florida Homes team of Lang Realty, and we’ll put the priorities of you and your family front and center to build you a strategy that feels the perfect fit.

✔️ Business continues to be strong, and it all starts with world class service — we’re so excited to have been featured in the Sun Sentinel newspaper, with this lovely article that ran in the Sunday, May 16th issue!

By: Amy Snook

Special to the Boca and Delray newspapers

Our world has changed so much in just a few months. For those of us fortunate enough to maintain our health during this crisis, we were forced to manage our lives in a very different manner.

We learned to work from home, we learned to balance home life with work with absolutely no escape for quiet time. We were forced to slow down and even developed some new skills out of necessity. Many of us are now Zoom experts, learned how telehealth works, learned to enhance our cooking, homeschooled our children, learned the importance of human interaction and friendship, and even learned how to workout at home. Buried in all of the sadness and dismay that came with COVID-19 were some very relevant and important life lessons about priorities.

The hope is that we all implement changes to our lives, for the better, and grow as a world moving forward. People in general are evaluating their lives and in particular where they are living their lives. They are looking at how best to protect their families and how best to survive in a catastrophe such as the one(s) we have been experiencing.

It therefore makes perfect sense that people from big cities are evaluating whether to remain living in the city or to move to the suburbs. Quarantine was difficult for everyone but for those of us in warm weather, we were afforded an opportunity to get out often for fresh air, and realized how important this is for our mental and physical well-being. It is not surprising that Realtors’ phones are ringing with Northerners looking to relocate to South Florida.

How do you evaluate where to live in a completely new state? This is where Realtors play an essential role in this relocation process.

Realtors are the homebuyers’ gateway to their new home. It is our job to get to know you and understand the lifestyle that works for you and your family. We need to educate the homeowner on the various cities and what each has to offer. So often we meet a buyer who starts out saying I “must” live near the beach but as we educate them on the options east, they quickly realize that they get much more house for the same price west and there are western communities with an easy, direct route to the beach. You can have it all if you make an informed decision. Looking for a golf club community but don’t want a large equity investment? Realtors can guide you to golf course communities that do not mandate membership making it an option not only for you but for a future buyer should you ever decide to move again.

It is a Realtor’s job to assist you in finding the right community and to protect you as you make your investment.

Providing walk through options for showings without a buyer physically having to be here to physically walk through is more important now than ever. As listing agents, we are adding the 360 tours, which allow potential buyers to “walk through” the home with the use of a mouse guiding the view as you virtually walk through the prospective home. For our buyers, if a particular property we are looking at does not offer at 360 tour – we are resourceful and utilizing technology to virtually walk you through all nooks of the home.

Partnering with the right Realtors is key to relocation.

Amy Snook, a 1990 graduate of the University of Maryland, is a partner in the All About Florida Homes team of Lang Realty, along with co-partner Noreen Payne of Delray Beach. She has been practicing real estate and title insurance for 17 years and is currently the Florida State Vice President for Women’s Council of Realtors. Amy is also a director of the Realtors Association of the Palm Beaches and Greater Fort Lauderdale and a director of Florida Realtors. She resides in Atlantis, Florida.

“Some buyers were waiting for the next recession, thinking home prices would fall again – but recessions aren’t created equal. The latest downturn exposed those myths.”- FloridaRealtors.orgBy: Russ Wiles

NEW YORK – The current economic downtown has been odd in so many ways. Why shouldn’t it expose some economic myths and misconceptions as unreliable, if not outright untrue?

When it comes to understanding the relationships involving home prices, bank deposits, interest rates and unemployment, many disconnects arise. Here are a few:

You might think that as the nation’s unemployment rate has spiked during this social-distancing recession, that would put pressure on home prices, forcing some owners to miss payments and discouraging buyers.

So far, that hasn’t been apparent. Home prices were up 2.5% on average this year through April, according to S&P CoreLogic Case-Shiller.

Low interest rates, which make homes more affordable, are one factor supporting prices. Also, stimulus and other government payments have enabled millions of Americans to meet their obligations. Plus, the economic slump has lasted only about four months so far, so the full impact may not have been felt yet. If the economy recovers strongly from here, negative housing fallout might not materialize in a big way.

Still, it does seem like the other shoe could drop. Fitch Ratings, the credit-rating agency, currently sees home prices nationally as 6.1% overvalued based on recent price increases, heightened unemployment and the possibility of lower incomes and rents. Values are most frothy in Nevada, Idaho, North Dakota, Texas and Arizona, Fitch said.

The degree to which housing might become more overvalued depends on the future path of unemployment and personal incomes, said Suzanne Mistretta, a Fitch senior director.

The company sees the U.S. unemployment rate easing to 7.8% next year from an average 10.3% in 2020. Though not approaching overvaluation levels of 20%-plus from 2005 to 2007, housing still could reach its highest level of overvaluation in a decade, Fitch warned.

Many people used to assume widening federal deficits would exert a crowding-out effect, pushing interest rates higher as the supply of debt mushroomed and private savings were siphoned from other investments. Few people seem to be focused on this connection anymore, given that interest rates keep dropping while Washington’s borrowing needs continue unabated.

One explanation for why the link doesn’t seem to work is the lack of inflation, as inflation and long-term interest rates tend to move together.

Another is the preference among investors for owning government bonds, which carry high credit ratings, during periods of heightened uncertainty. When things get tough, investors get nervous. They snap up government bonds with preservation of capital, not yield, as the primary goal.

As the Tax Foundation noted in a 2016 report, some economists had been suggesting that budget deficits reduce economic growth by boosting interest rates and diverting private saving toward the purchase of government debt. But in practice, “It has been hard to find an empirical link between deficits and increased interest rates or reduced investment,” the group concluded.

Rates are even lower, and deficits higher, today.

You would think that with bank deposit accounts, money-market mutual funds and other risk-averse instruments yielding next to nothing, investors would be ready to move their money elsewhere. But so far, millions of people are willing to accept virtually no yield so long as their assets remain safe.

Bank deposits spiked by $1.2 trillion in the first quarter, the most recent figure tracked by the Federal Deposit Insurance Corp. That was nearly four times the size of any other quarterly deposit gain over the past decade. Americans also have been flocking to money-market funds and other risk-averse instruments. Money-fund assets are up more than $1 trillion so far this year, reports Money Fund Intelligence newsletter.

It’s not like risky stock-market investments have been faring all that poorly. The broad market was up roughly 43% from its recent low in late March through July 9. But for a lot of people, safety reigns supreme – and they’re willing to pay a price for it, in low returns.

Before the recession, the vast majority of people with bachelor’s degrees who wanted jobs could get them. As recently as March, the national unemployment rate for college graduates was 2.5%. That was well below comparable figures for less-educated Americans, such as the 4.4% rate for people with only a high school diploma.

College graduates also typically earn more – $1,248 a week on average for holders of bachelor’s degrees only, compared with $746 for those with a high school diploma only, according to a May update by the Bureau of Labor Statistics.

However, that picture has changed a bit amid this coronavirus-induced economic slump. The unemployment rate for college grads more than tripled overnight to 8.4% in April and 7.4% in May before easing to 6.9% in June, according to the Department of Labor.

That’s still well below comparable rates for less-educated groups, such as the 12.1% June unemployment rate for high-school graduates. (The department also tracks workers based on whether they have some high school attainment and some college.)

Still, it lays to rest, at least temporarily, the notion that college graduates are immune from layoffs or other career bumps, especially amid an economic backdrop as strange as this one has been.

You might think now would be a tough time to save money. During recessions and other periods of high unemployment, more people are financially stressed, the reasoning goes. It would be the time for many individuals to lean on their savings to help make ends meet.

That might be the case for a lot of people, but it certainly doesn’t tell the whole story. The nation’s savings rate often has climbed during recessions, and while real-time numbers aren’t available yet, that could be the case again.

Part of this might reflect a reluctance or lack of opportunity to spend money. Think how much you have saved in recent months by eating at home rather than at restaurants, not taking vacations and so on. Perhaps many people also are making a genuine effort to get their budgets under control by putting off various types of spending.

It’s not just individuals, either. A March survey of corporate finance officers conducted by the Association for Financial Professionals noted the largest increase in three years of businesses holding short-term investments at banks.

![]()

Amy speaks to friends,clients, and anyone looking for some answers as to how we can step up our game to make technology helpful and exciting. With Virtual tours and new technology anything is possible.